Mahogany Place III by DMCI Homes

Center of business and leisure within easy reach

A DMCI Homes signature community that places you at the quiet side of the city, far from the hustle and bustle of the city yet still conveniently close for you to experience the benefits of in-city living. Here, travel time and traffic-related stress significantly drops as the country's growing financial and entertainment districts - Bonifacio Global City and Makati - are now just a few minutes drive.

Exclusivity coupled with Asian elegance

One of the most exclusive subdivision developments with only 298 home units spread across 8-hectares of land, featuring a distinct Asian contemporary design theme highlighted by Asian-inspired rooflines and façade designs in subtle color tones contributing to create a warm look and a relaxing feel.

High on space and greens

Mahogany Place III can hold claim to being the home village having the widest, pedestrian-friendly open spaces dedicated to tree-shaded parks, verdant gardens and landscaped amenities area offering a calming neighborhood setting ideal for active recreation, family interaction and private relaxation.

The Heartland

Mahogany Place III's Clubhouse will surely lure you from your home to the outdoors. Featuring a country club-like design, it houses a wide array of rest and recreational amenities that cater to your various needs. We have designed and created a feel of it being an extension of your home - a place where you could celebrate life's precious moments and remember it by.

Hospitality like no other

If hotels have their Concierge desks, we have our very own Property Concierge Office. Located inside the village, our Concierge officers will be responsible for keeping you and your loved ones safe, secured and pampered. They'll provide you with an array of first-class and reliable services not found at any other village development.

Price range: P11M - P30M

Location

Ideally located in progressive Taguig City, Mahogany Place III is accessible via C-5 and only a few minutes from Bonifacio Global City and the Makati Central Business District.

How to get there

Via C-5 (From Libis) - Exit at Bayani Road tunnel (near Heritage Park) to make a U-turn to C-5 Northbound lane. Drive straight to Petron-BCDA then make a right to Padre Diego Silang Road. Follow the road and turn right to Levi Mariano Ave. Take another right at Acacia Road, corner of Rosewood Pointe, then drive straight until you reach Mahogany Place III.

Via EDSA (From SLEX) - From EDSA, turn right to McKinley Road. Take Lawton Ave. then turn left to Bayani Road (Heritage Park). Pass thru C-5 tunnel to enter C-5 Northbound lane. Drive straight to Petron-BCDA then make a right to Padre Diego Silang Road. Follow the road and turn right to Levi Mariano Ave. Take another right at Acacia Road, corner of Rosewood Pointe, then drive straight until you reach Mahogany Place III.

Area Distances

A. Business Districts

- BGC - 3.65 Km

- Makati - 7.5 Km

- Ortigas - 8.14 Km

B. Commercial

- Market! Market! - 3.65 Km

- Bonifacio High Street - 4.03 Km

- Greenbelt - 7.61 Km

- Tiendesitas - 8.78 Km

C. Schools

- International School - 4.06 Km

- British School - 4.07 Km

- Colegio de San Agustin - 5.14 Km

- Assumption College - 8.01 Km

D. Hospitals

- St. Luke's Hospital - BGC - 4.4 Km

- Makati Medical Center - 9.18 Km

Site Development Plan

Amenities and Facilities

Outdoor Amenities

- Adult pool

- Kiddie pool

- Pool deck

- Picnic grove

- Children's playground

- Sandbox

- Basketball / Tennis court

- Parks and gardens

- Landscaped amphitheater with plaza

Clubhouse Amenities

- Lobby lounge area

- Main function hall with bar and kitchen

- Sauna

- Poolside dining

- Mini-mart

- Mini-theater

- Dance studio

- Game room

- Fitness gym

- Refreshment area

- 2 nd Floor lounge area

- View deck

Facilities

- Guarded grand entrance gate

- 24-hour security

- Water station

- Overhead water tank and cistern

- Garbage collection facilities

- Back-up generator for the Clubhouse

- Wi-Fi accessibility at the Clubhouse

Amenities

Tree-lined Streets

Parks and Gardens

Amphitheater

Adult and Kiddie Pools

Poolside Dining

Playground

Mini-theater

House Models

Ariana

- Lot area (approx.) : 240.00 SQ.M.

- Gross Floor area (approx.) : 378.80 SQ.M.

Ground Floor

Second Floor

Third Floor

Upgrade Options

--------------------------------------------------------------------------------------------------------------------------------------------

Bela

- Lot area (approx.) : 240.00 SQ.M.

- Gross Floor area (approx.) : 307.10 SQ.M.

Ground Floor

Second Floor

--------------------------------------------------------------------------------------------------------------------------------------------

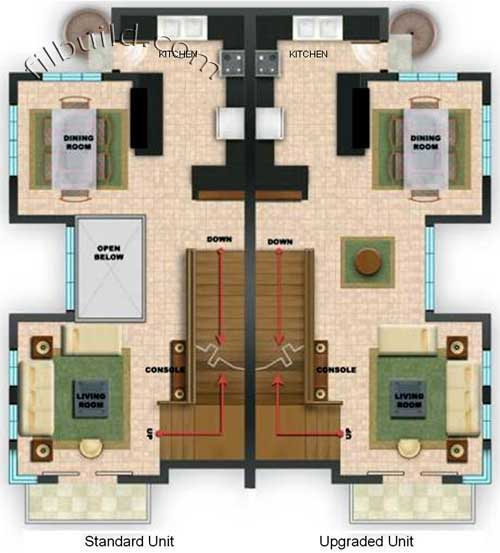

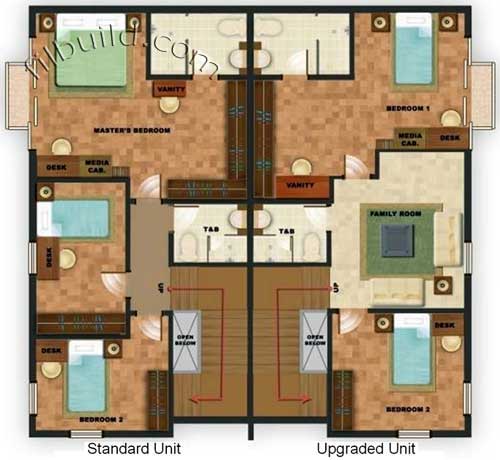

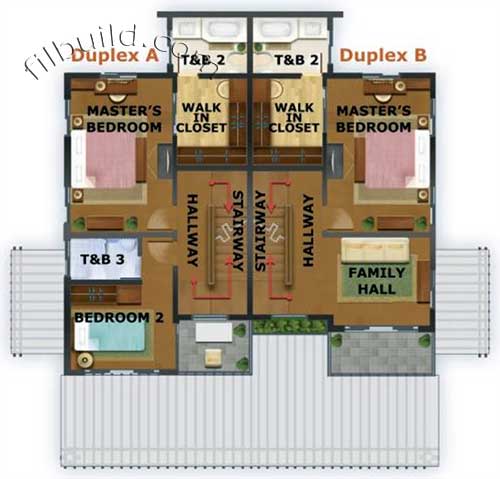

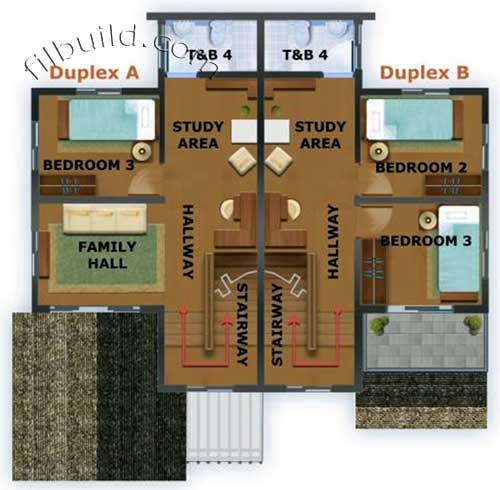

Helena

- Lot area (approx.) : 120.00 SQ.M.

- Unit A - Gross Floor area (approx.) : 251.00 SQ.M.

- Unit B - Gross Floor area (approx.) : 251.00 SQ.M.

Ground Floor

Second Floor

Third Floor

Upgrade Options

--------------------------------------------------------------------------------------------------------------------------------------------

Tamara

- Lot area (approx.) : 120.00 SQ.M.

- Unit A - Gross Floor area (approx.) : 206.60 SQ.M.

- Unit B - Gross Floor area (approx.) : 213.50 SQ.M.

Ground Floor

Second Floor

Third Floor

Home Features

Bela and Tamara

- Asian contemporary-themed

- Large windows and door openings

- Landscaped frontage

- Wide hallways on upper floors

- Walk-in closet and bathtub in the Master's Bedroom

- With built-in closets in all bedrooms (except in the maid's and driver's room)

- With a separate balcony in the Master's bedroom (Bela only)

- Dining extends to a garden

- With provisions for water heater in all T&B (except in the maid's and driver's room)

- Multiple car garage

Helena and Ariana

- Designed by award winning Architect Dan Lichauco

- Modern contemporary-inspired

- Living spaces flow to the outdoor areas such as lanais, decks or balconies

- Efficient energy saving designs

- Available upgrade options

- Separate entrance for service staff

- Double height ceilings in the living areas

- Provision for split-type kitchen

- All rooms are Internet-ready

- Multiple car garage

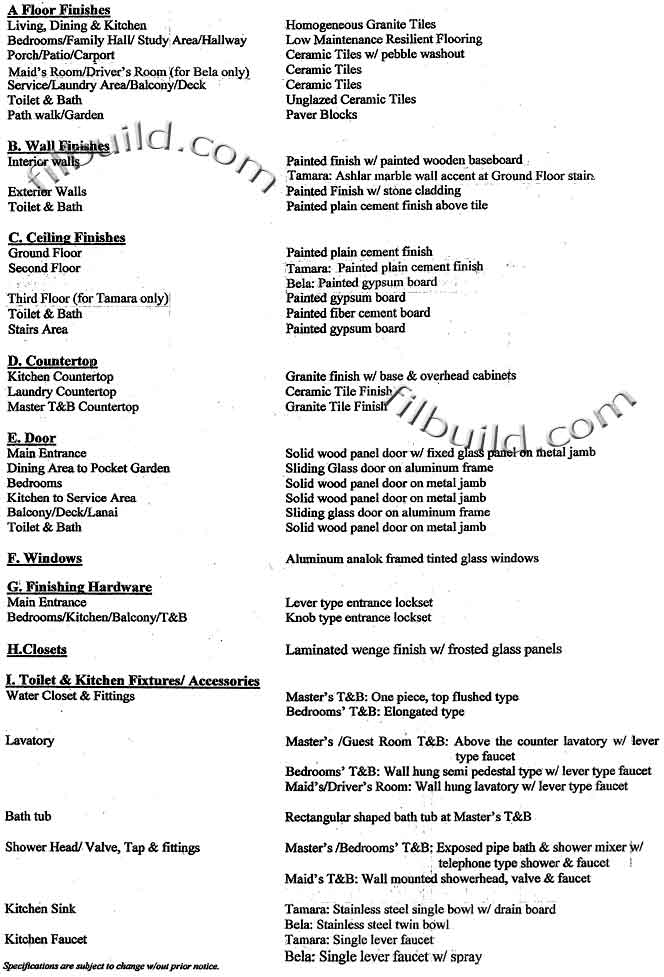

Turnover Finishes

Construction Actual Photos

August 2008

Ariana Model House

Clubhouse

May 2008

Entrance Gate

Main Road past the Entrance Gate

Clubhouse

Rotunda

Financing

In-house Financing

Note: For DP more than 40%, the applicable discount and factor rates shall be based on 40% DP also.

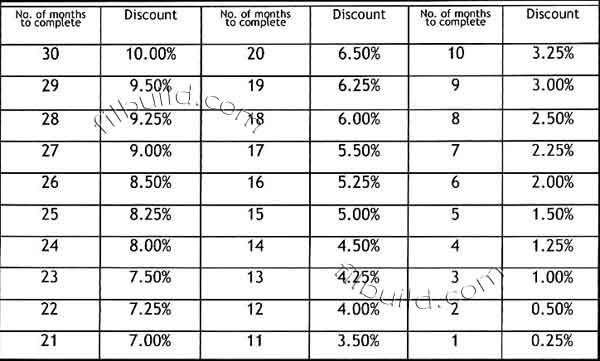

Additional Discount for Spot Cash Payment During Construction Period

For projects with more than 30 months construction period, applicable discount shall be maximum of 10%. These are only applicable to any spot cash payments during construction period. In the case of spot downpayment or partial cash payments, additional discount will be applied on the cash portion only.

Direct Bank Financing

- Applicable to Accredited Banks only

- If thru NON Accredited Banks - should avail of In-house Financing up to loan drawdown

Accredited Banks

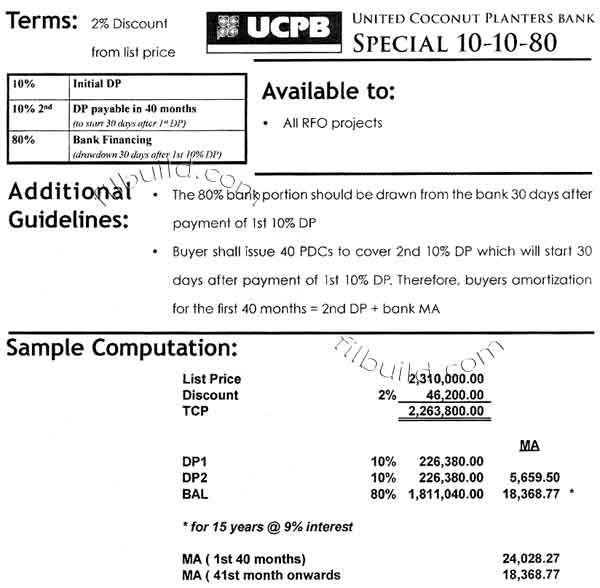

- United Coconut Planters Bank

- BDO/EPCIB

- Union Bank/IBank

- BPI Family Savings Bank

General Terms

- Maximum Loan Amount = 80% of TCP (depending on the result of Credit Investigation)

- Availability of Title & TD = available

- Condominium = RFO

- House and Lot = 100% completed

- Equity = fully paid

Addendum to CTS

- For direct bank financing, buyer shall sign additional document/undertaking which shall form part of the Contract to Sell

- Undertaking states that buyer shall automatically convert to In-house financing in the following instances:

- Disapproval by the bank

- Delay in processing of documents/loan drawdown caused by the buyer

Transfer Fees

- Should be collected prior to loan release

- DMCI will process the Title Transfer. Client does NOT have the option to process Title Transfer

- Details & Computations are as follows:

- Documentary Stamp Tax (DST) - payments made to Bureau of Internal revenue (1.5% of TCP or Zonal Value whichever is higher)

- Transfer Fees - taxes paid to City Treasurer's Office (0.5%)

- Registration Fees - dues paid to the Registry of Deeds (RD)

- Assurance Fund - 1/4% of 1% required by law for every transferred title

- Processing Fees - miscellaneous; e.i., notarial fees, administrative fees, etc.

- Real Property tax - billed upon acceptance of the unit

Regular Bank Financing

Available to

- All Ready For Occupancy (RFO) projects

- Non-RFO medium-rise projects

Accredited Banks

- United Coconut Planters Bank

- BDO/EPCIB

- Union Bank/IBank

- BPI Family Savings Bank

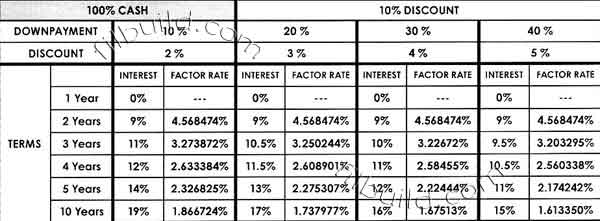

Discount Rates

| 10% DP, 90% BF | 2% |

| 20% DP, 80% BF | 3% |

| 30% DP, 70% BF | 4% |

| 40% DP, 60% BF | 5% |

Sample Computation

Requirements

Personal Data & Income

If Employed (within the Philippines)

- Certificate of Employment (COE) indicating annual salary and position

- Latest Income Tax Return (ITR)

- Pay slips (last 2 months)

- Proof of Billing Address (Meralco, credit card, etc.)

If Overseas Filipino Worker (OFW)

- POEA authenticated contract (seaman)

- COE authenticated by Philippine Consulate (direct-hired)

If Self-Employed

- Business Name (DTI or SEC Registration)

- Articles of Incorporation and By-laws with SEC Registration Certificates

- List of Trade References (at least 3 names & telephone numbers of major suppliers/customers)

- Audited Financial Statements for the past two years

- Bank Statement for the last six months

- Proof of Billing address (Meralco, credit card, etc.)

If Practicing Doctor

- Clinic address/es and schedule

- Bank Statement for the last six months

If income is from Rental or Properties

- List of tenants and rental amounts

- Complete address/es of properties being rented

- Bank Statement for the last six months

Developer's Requirements

- Issue post dated checks (PDC) payable to the Developer to cover down payment/equity portion

- Settle unpaid equities

- Settle transfer fees to the Developer/Seller

- Sign Contract to Sell/Deed of Sale

Bank Requirements

- Client to express conformity to the Letter of Guarantee (LOG)

- Client to sign the loan documents (Deed of Assignment, Promissory Note, Real Estate Mortgage, Special Power if Attorney, etc.)

- Submit the post-approval requirements of preferred bank, such as

- Post-dated checks

- Mortgage Redemption Insurance (MRI)

- Insurance of the property to be financed

- For Condominiums - Fire/Earthquake Insurance endorsement, Policy & Photocopy of the Official Receipt can be obtained from the Office of the Property Manager

- For Completed House and Lot, Townhouse - insurance should be obtained from a reputable/accredited insurance company

Collateral

Clear photocopy sets of Transfer Certificate of Title (including blank pages with the book and page/volume number indicated on the front page)

For Condominium

- Photocopy of Condominium Certificate of Title (CCT)

- Certificate of Consent and Updated payment of Monthly Dues from Condo Corp.

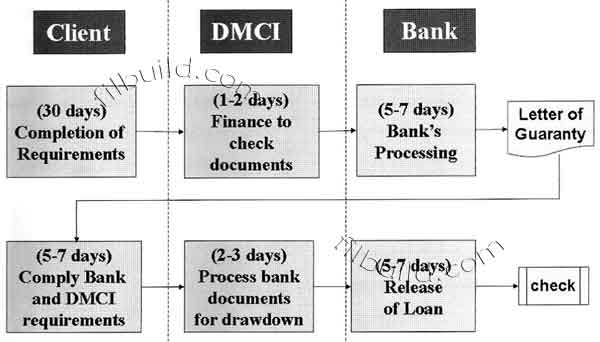

Bank Financing Cycle

Reminders

- Documents should be submitted to Finance Department within thirty 30 days from reservation date. Failure to submit on time shall automatically convert the account to In-House financing.

- Target drawdown date is within 60 days from reservation date or 30 days after full payment of required DP.

- Turnover of unit shall be after loan drawdown.

Bank Financing Process

- The process starts with the client's intent to finance his/her outstanding loan with DMCI thru the bank.

- The client prepares the necessary documents for submission to bank.

- The bank performs the necessary credit investigations & background checks & documentation.

- The bank then approves the loan.

- The bank issues a letter of guarantee & deed of undertaking.

- Finance assistant reviews the documentation and clarifies with the client issues regarding his account.

- Finance assistant endorses the documents to the Department Head for final review and signing; then forwards the document to the authorized signatories to sign signifying DMCI's conforme.

- Authorized signatory signs the LOG & DOU.

- Reproduction of the LOG and DOU.

- A copy of the LOG and DOU is placed on file.

- Another copy of the LOG and DOU shall be forwarded to DOCS CONTROL group for preparation of DOAS.

- Collate the documents.

- Prepare documents for transmittal to Bank.

- Bank processing.

- Determine if accredited bank or if documents can be undertaken.

- If not an accredited bank, Finance Assistant shall wait for the compliance of Legal Department and then the Bank releases the proceeds of the loan.

- If accredited Bank, bank will immediately release proceeds of the loan subject to an undertaking. Compliance by Legal Department.

- Endorse the account (after drawdown) to Billing and Collection for Final Billing.

Pag-IBIG Financing

The Pag-IBIG housing loan may be used to finance any of the following:

- Purchase of a fully developed lot

- Purchase of a residential house and lot, townhouse or condominium unit

- Construction or completion of a residential unit on a lot owned by the member

- Purchase of a lot and construction of a residential unit thereon

- Home improvement

- Refinancing of an existing loan

- Combination of loan purposes

- Purchase of lot and construction at a residential unit thereon

- Purchase of a residential unit, with home improvement

- Refinancing of an existing mortgage with home improvement

- Refinancing of an existing mortgage, specifically a lot loan, with construction of a residential unit thereon

Borrower Eligibility

- Pag-IBIG I and Fag-IBIG II Program

- Member for at least 24 months at the time of loan application

- Pag-IBIG Overseas Program (POP)

- Member for at least 24 months at the time of loan application

- Not more than 70 years old at loan maturity and must be insurable

- Has the legal capacity to acquire and encumber real property

- Has passed satisfactory background/credit and employment/business checks

- Has no outstanding Pag-IBIG housing loan

- Has no outstanding Pag-IBIG multipurpose loan in arrears at the time of loan application

- Had no Pag-IBIG housing loan that was foreclosed, cancelled, bought back, or subjected to dacion en pago.

Loan Amount

Maximum of P2M, which shall be based on the lowest of the following:

- Capacity to pay (40% of Net Disposable Income)

- The Member's actual need

- His loan entitlement based on member contribution

- Loan-to-collateral ratio

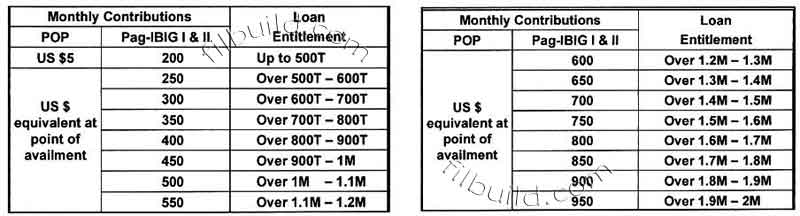

Loan Entitlement Based on Pag-Ibig Contributions

Loan Entitlement Based on Capacity to Pay

Shall be limited to an amount for which the monthly amortization shall not exceed 40% of the member's Net Disposable Income (NDI).

Tacking Provision

Maximum of three (3) qualified Pag-Ibig members who are related within the first civil degree of consanguinity or affinity. Ex:

- Married - spouse, parents/parents-in-law, children

- Single - parents

Interest Rate

| Loan Package | Interest Rate |

| Up to 300T | 6% |

| Over 300T - 750T | 7% |

| Over 750T - 2M | 10.5% |

Repricing

| Loan Package | Interest Rate |

| Over 300T - 750T | 9% |

| Over 750T - 2M | 12.5% |

- For loans up to P300K Pag-IBIG Fund may reprice the interest rate every 3yrs provided that it shall not exceed the original rate.

- For loans over P300K up to 2M, Pag-IBIG Fund shall reprice the interest rate of the loans every three (3) years at the rates based on prevailing market rates at point of repricing, which shall not be lower than the original rates.

Loan Term

Membership Program Pag-IBIG I, II & POP

| Loan Bracket | Term |

| Up to 2M | Maximum of 30 years |

- Shall not exceed the difference between the principal borrower's age at the time of loan application and age seventy (70).

- Borrower shall be allowed to lengthen or shorten the loan term only once during the life of the loan.

Insurance

Mortgage Redemption Insurance (MRI)

- Interim Coverage - based from the issuance of Notice of Approval (NOA) or Letter of Guaranty (LOG) by HDMF.

- Regular Coverage - effective on the date of loan take out.

Fire and Allied Perils Insurance

- Covers the amount equivalent to the appraised value of the residential unit or the loan amount, whichever is lower.

Second Availment

A Pag-IBIG member may avail himself of a second Pag-IBIG housing loan provided he has fully paid his first housing loan, whether as a principal borrower or as a co-borrower.

Additional Loan

A qualified Pag-IBIG member who has an existing housing loan may avail himself of an additional housing loan for the following purposes:

- House construction or improvement of a house constructed on a lot purchased through a

Pag-IBIG housing loan. - Home improvement, under the terms and conditions of the Good Payor Home Improvement Loan Program.

Loan Charges

- Processing Fee - P3,000

- P1,000 - upon filing of HLA, non-refundable

- P2,000 - upon loan take-out

- One year Pre-payment Insurance - to be deducted from the loan proceeds

- Interim Mortgage Redemption Insurance - to be deducted from the loan proceeds (6 mos.)

- One (1) month advanced monthly amortization (without buyback or Window 2 & Retail Acct)

- Retention Fee (CTS) is the amount retained to cover the transfer of TCT under the borrower's name:

- 5.0% - for loans up to 180T

- 6.0% - for loans over 180T to 500T

- 7.0% - for loans over 500T to 1M

- 7.5% - for loans over 1M to 2M

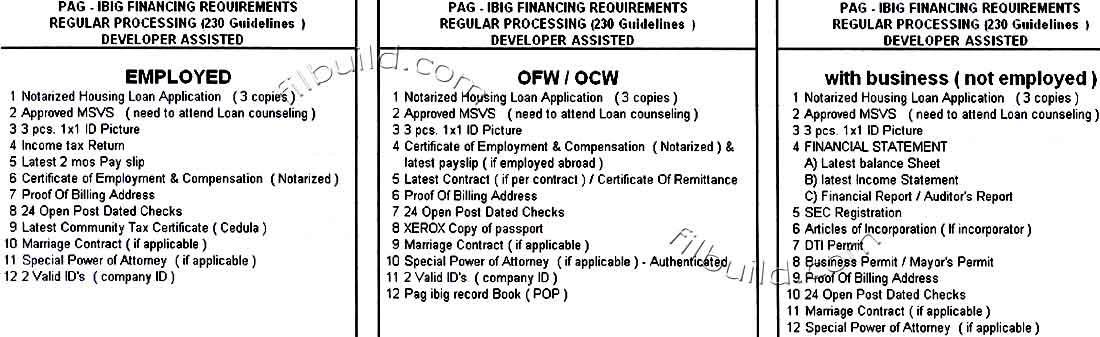

Pag-IBIG Financing Requirements

About the Developer

DMCI Homes is the country's first Triple A builder/developer of premium quality, urban-friendly, fully serviced communities for the underserved young families of modest income that aspire to live comfortably near their place of work, of study and of leisure.

For the growing family with limited options in an increasingly challenging urban living situation, we at DMCI Homes are here for you.

At DMCI Homes, we build more than condominiums and houses, we build communities that respond to the needs and wants of the Filipino family. Residential communities by DMCI Homes provide what is healthy and suitable for the general well-being of individuals and growing families.

Beyond reliable structures, DMCI Homes' residential communities provide a solid foundation where a family may create a place of their own and grow in a space they can truly call home, now and for years to come.

DMCI Homes is a 100%-owned subsidiary of DMCI Holdings, Inc.

Contact Us

DMCI Homes

Corporate Center

1321 Apolinario St.

Bangkal, Makati City

For Local Sales Inquiries

Tel: (632) 324-8888

dmcihomespostman@gmail.com

For International Sales Inquiries

Mobile: (63) (917) 880-8800

dmciinternationalwebsite@gmail.com

Accredited Brokers/Agents:

Contact: Ralph Alcazar Jr., REB ZAM 13-07(R)

Mobile: +63 908 896 5800

Email: alcazartm@gmail.com

Attention Our Valued Users

The particulars and visuals shown herein are intended to give a general idea of the project and as such are not to be relied upon as statements of fact. While such particulars and details on present plans which have been prepared with utmost care and given in good faith, buyers are invited to verify their factual correctness and subsequent changes, if any. The contents herein are subject to change without prior notice and do not constitute part of an offer or contract. For more information please see our Terms of Use.

Terms of Use/Privacy Policy Advertise